This Stock Could Surge As Mining Analysts Predict Significant Copper Profits By 2027

At Capital Rankings, we pride ourselves on finding winners before the market.

In a prior article, the stock we selected soared to a split-adjusted high of $16.50.3

Before that, another featured company — earlier in its development cycle — reached an all-time high of $20.43 on a split-adjusted basis.3

We are writing again today because we have found perhaps the best trade setup right now, one that could net significant returns for our readers who take action early.

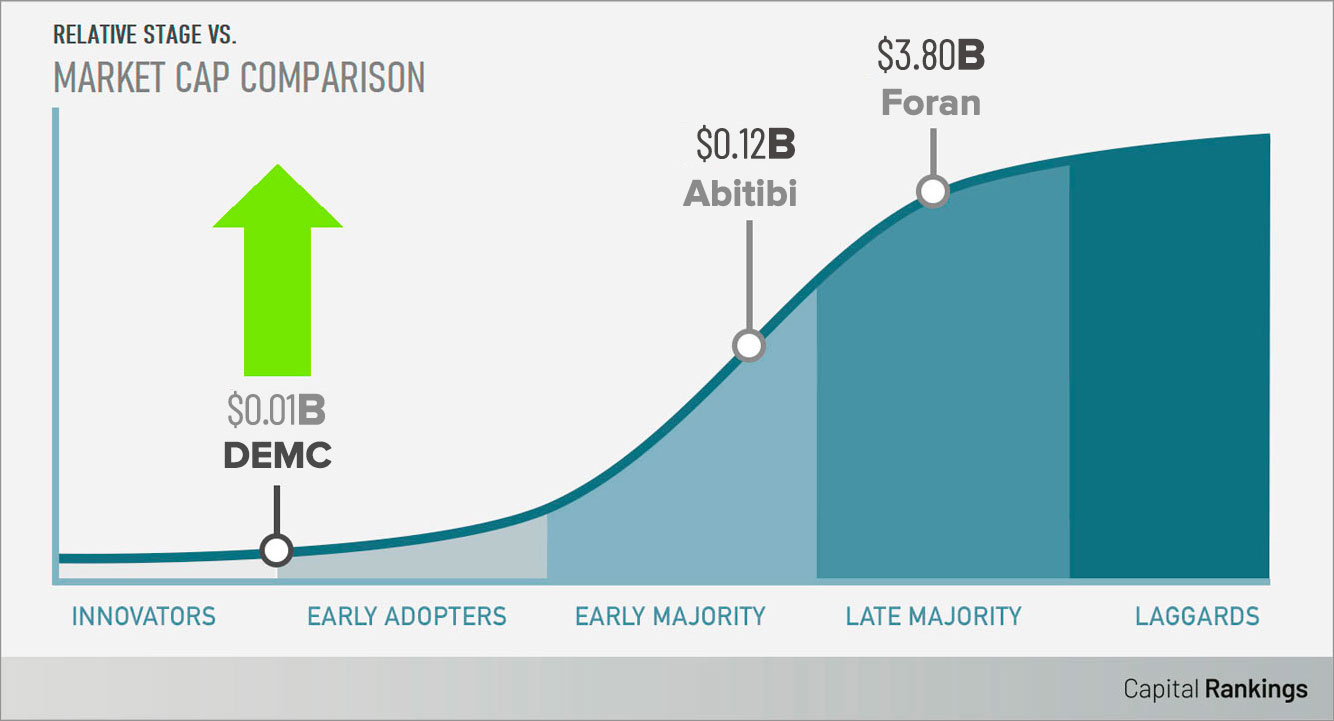

Put simply, Discovery Energy Metals (CSE: DEMC) could present the highest-potential opportunity we’ve seen in years as the copper market takes flight to record-highs.4

Before we get into the details of why Discovery Energy Metals (CSE: DEMC) is perhaps the best stock to buy in the copper mining sector today, it’s important to understand the context of the broader copper market and how it provides a solid basis for investment in 2026.

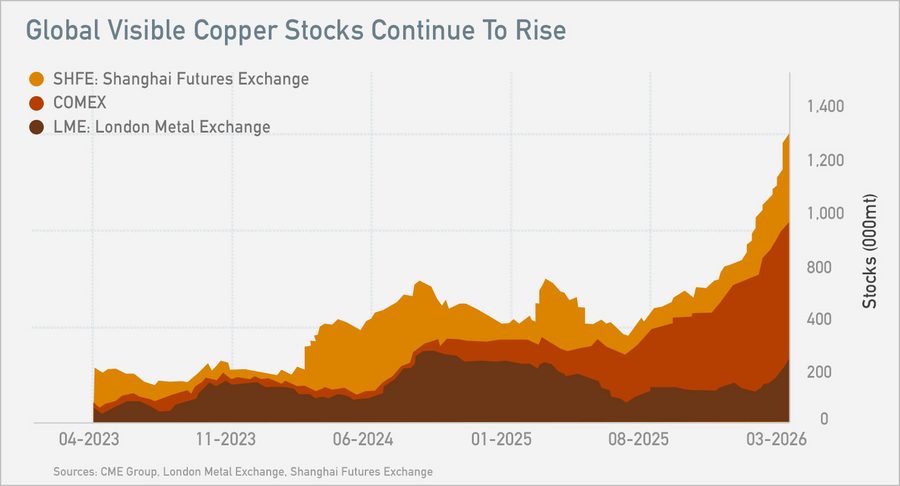

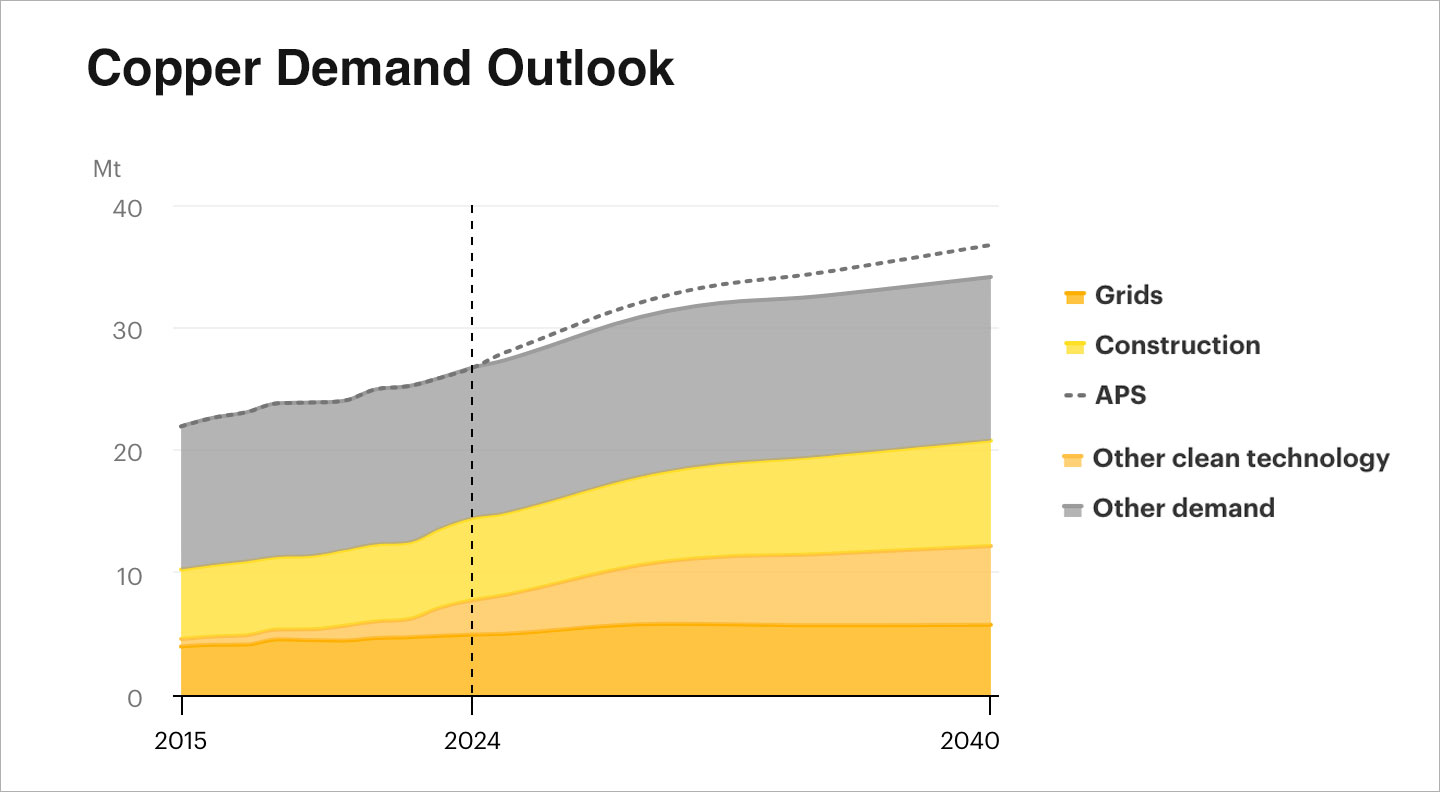

You see, in today’s market conditions, copper is king and higher record-breaking prices1 are setting the stage for big winners.2

Absolutely massive returns are made in young copper exploration companies when they are small, before the large funds can get their hands on them. This strategy has proven its worth over the years, with returns exceeding +772% on invested capital.3

Many analysts today expect copper to soar past $15,000 per metric ton in the months ahead.5,6,7 If history repeats itself, investors who are taking major positions in the right junior copper miners now could reap massive profits by 2027.8

For our large experienced investors, the entire 116-page research package on the copper market is available here.

Historic Prices Fueled by Record Demand

Andurand, the legendary commodity trader, recently revealed in a FT article: copper to surpass US$40,000/mt by 2030.8

Andurand, the legendary commodity trader, recently revealed in a FT article: copper to surpass US$40,000/mt by 2030.8

Based on target prices set by some of the world’s top investment firms, this copper trend could be one for the history books.9 Even billionaire founder of Ivan Mines ($18B market cap), Mr. Robert Friedland, fully expects copper prices will double from here.

Buyout After Buyout: A Race For Supply

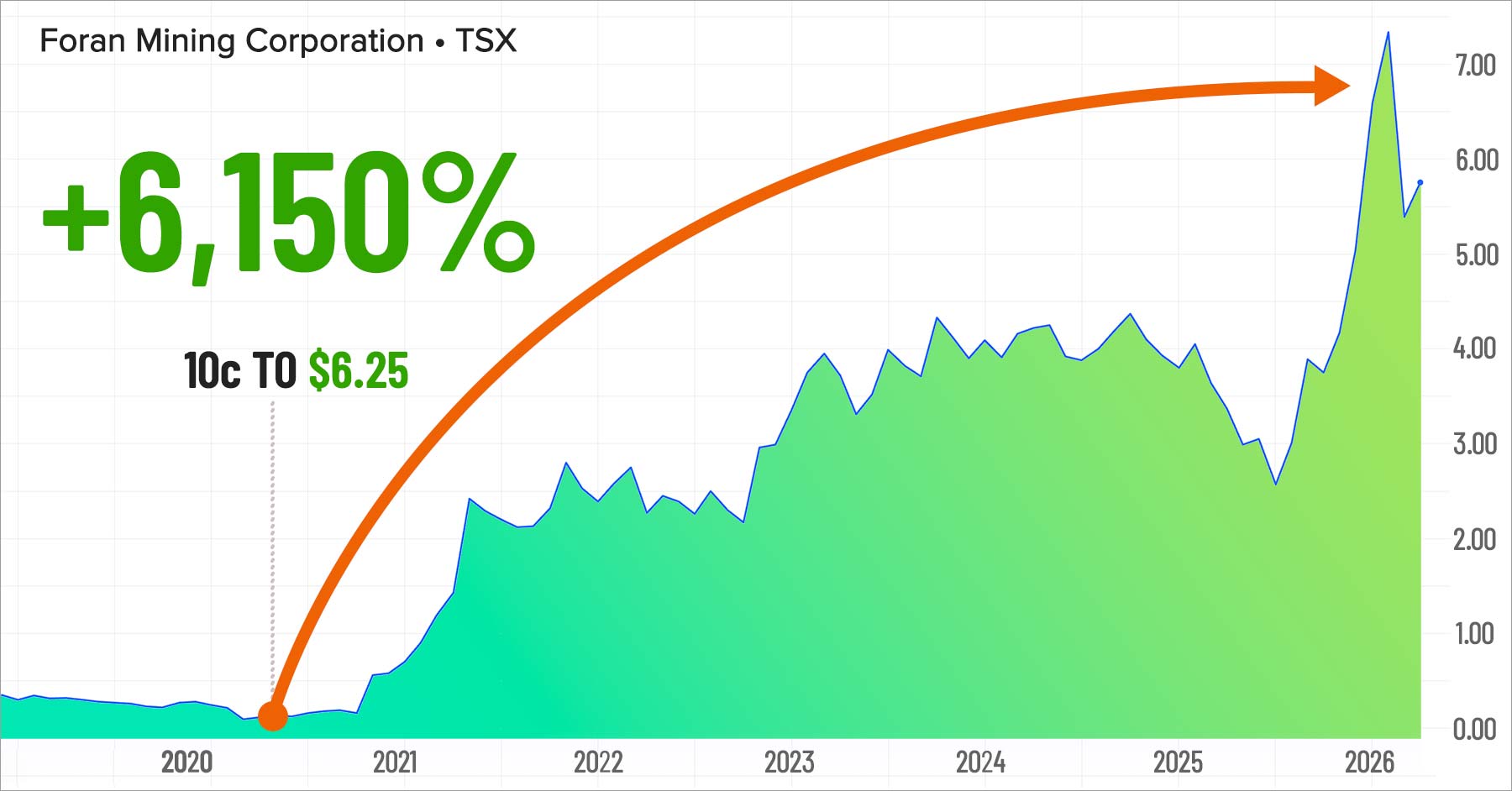

Before it announced the results of its drilling, in April of 2020, Foran Mining’s shares could be purchased for just $0.10. By the time the buyout came around, the stock had soared far beyond $6 per share. Investors who logged into their accounts on the morning of January 20th this year were greeted with a trading price of $6.25 per share.11 Later, the price soared even higher. It’s become a prime case study of what can happen when you invest in the right junior copper miner before the majors show up with a cheque.

From the April 2020 placement to the deal consideration, investors saw an enormous +6,150% return.12 A $10,000 position held through the April 14, 2026 deal close became approximately $625,000.13

Looking at the chart below of Foran, it’s hard not to draw parallels to the current trading and corporate development stage of Discovery Energy Metals (CSE: DEMC), a junior company operating in the same area with similar corporate milestones ahead.

Prior to the takeout, shares of Foran Mining could be purchased by investors for $0.10. Within one exploration cycle, the stock soared above $6.00 per share, reaping large immediate profits for investors who purchased before the run.

The Biggest Discoveries May Yet Be Found

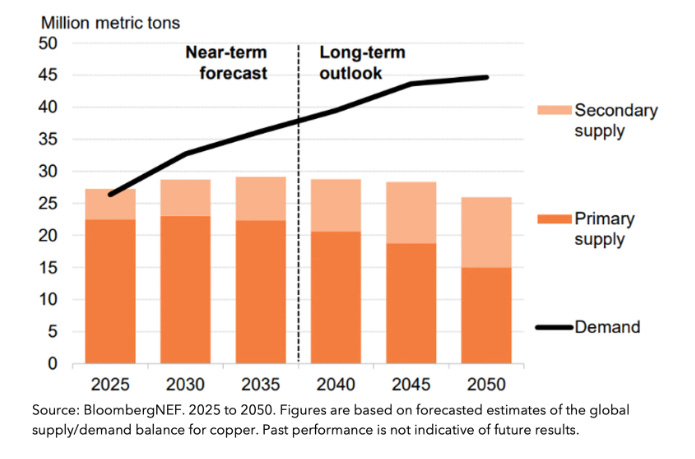

Despite decades of drilling and new mines coming online, the world is running short of copper. Head grades have declined approximately 40% since 1991.14 Only 14 of the 239 copper deposits brought into development since 2013 qualify as genuine new discoveries.15 And even when new discoveries are found, the development timeline to first production can stretch to 25 years.16

Copper has now been added to the U.S. 2025 Critical Minerals list,17 and the IEA has warned of a ~30% supply gap by 2035 between announced projects and projected demand.18 The International Copper Study Group projects a 150,000-tonne deficit in 2026.19

Global copper mine production was 22.8 million tonnes in 2024; on current project pipelines, output could decline below 19 million tonnes by 2035 — a shortfall measured in millions of tonnes per year at the moment electrification demand is peaking.20

Both Eldorado Gold (NYSE Listed, $5B market cap), after closing its $3.8 billion Foran acquisition21, and Hudbay Minerals (NYSE Listed, $4B market cap), after closing its $1.48 billion Arizona Sonoran acquisition22, are now larger and hungrier for replacement pounds in jurisdictions like British Columbia and Nevada.

The key here is that Discovery Energy Metals (CSE: DEMC) is not only sitting within these target jurisdictions, it’s trading at a fraction of these behemoth miners,23 presenting large upside to early investors in the event of a major discovery (more on this below).

Finding The Next Big Potential Winner

One of the best ways to benefit from the tightening situation in copper is to look to some of the junior players positioning themselves in the right districts at the right time. But rather than invest in a company that has already gone up, such as Foran before the takeout, there’s much greater opportunity for out-sized returns by investing in an emerging player that has yet to have its big run — a company like Discovery Energy Metals (CSE: DEMC).

Discovery Energy Metals (CSE: DEMC)‘s market capitalization is only a fraction of the larger copper explorers re-rated this cycle. This naturally presents a greater upside in the event of further copper-price strength and any surprise drill results from its exploration activities.

If the company were to reach anywhere near the takeout market capitalization of Foran, given the tight share structure of 76.7M shares outstanding24, the implied market-cap move would be enormous. That is arithmetic, not a forecast. And while there’s no guarantee of that happening, it’s illustrative of the point that buying a junior with a tight share structure can quickly translate to windfall returns if an investment is placed in the right company before a major discovery is confirmed.

We use the word “confirmed” because the situation with Discovery Energy Metals (CSE: DEMC) is frankly rather unique. It has to do with the geography and its surrounding neighbors — neighbors whose properties have historically produced, have been bought by majors for nine- and ten-figure sums, or are actively being funded for development. And it’s these same mineralized belts that extend right across the very same ground that Discovery Energy Metals has secured interests in.25,38 Now, it’s possible that the mineralization of these neighboring discoveries, past producers, or deposits currently attracting major-company capital may not extend onto Discovery Energy Metals‘s ground at all. Legally, you have to say that and it’s illegal to say anything else until it’s fully confirmed by an NI 43-101 compliant technical study. But that seems rather unlikely given the geological setting.

And in the world of investing, like poker, it’s all about the probability of your hand. Investors who wait for the “sure thing” will be buying at the highs. It’s the investors who take the risk, buying before the confirmation, that position themselves to see the upside. From everything we see, it appears rather probable that Discovery Energy Metals (CSE: DEMC) is sitting on a royal flush here. For the details, and to decide for yourself what the evidence points toward, you’ll have to keep reading this article.

We recommend printing this article for your own reference while you conduct your due diligence to verify for yourself what all these signs point toward. If we’re right about this situation, this article may become one of the most important things you read all year.

The Right Spot: Surrounded By Winners

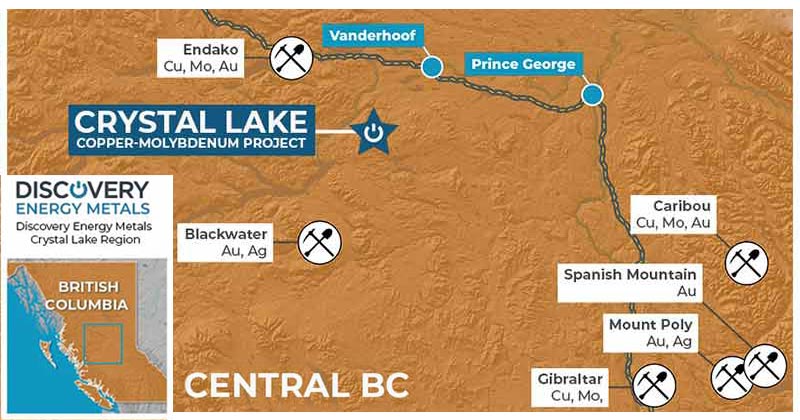

Discovery Energy Metals (CSE: DEMC) finds itself in an enviable position within North America’s mining landscape, neighbored by significant industry players and lucrative operations. Perhaps the biggest sign of what might be to come is at the Crystal Lake Copper-Molybdenum Project, its flagship property in central British Columbia sitting in a well-established mining jurisdiction with year-round road access and is approximately 34 km south of Fort Fraser, BC, covering eight contiguous mineral claims totaling approximately 5,283 hectares.28

Past work has already returned grab samples up to 0.70% copper, with the Raven Showing grab at 7,577 ppm Cu (~0.76%) plus accompanying silver and gold values,29 and historical work has outlined a roughly 2.3-kilometre magnetic porphyry target from Holler Lake to Bennett Lake.30 It’s a rare opportunity when you can buy a company early at a porphyry Cu-Mo target of that scale in a mature BC mining district where past operators have drilled ore-grade copper in grab samples on surface and although that is no guarantee of what drilling will find at depth, it’s certainly a sign you don’t want to ignore.

Of additional note, its ESN Project sits along the same belt that hosts Kinross Gold’s Bald Mountain gold mine, a Carlin-type system Kinross acquired from Barrick Gold for US$610 million in January 2016.26 That is a nine-figure major-producer cheque written for commodity-aligned exposure in the same belt Discovery Energy Metals is claiming.

One only needs to glimpse at the historical success of the Battle Mountain and Bald Mountain trend to understand how meaningful a major’s presence in the area is. Kinross has spent over a decade operating along this gold trend, demonstrating that this is a belt that keeps attracting capital. Discovery Energy Metals (CSE: DEMC) is positioning with 33 unpatented lode claims covering approximately 660 acres in that very same belt.27

Even more impressive, is that Discovery Energy Metals (CSE: DEMC)‘s Koster Dam Joint Venture in south-central British Columbia — 9 claims totaling 4,535 hectares, held 45% by Discovery Energy Metals with Cariboo Rose Resources as managing operator — is contiguous with and approximately 7 kilometres north of the former-producing Blackdome gold-silver mine.31 The very same structural corridor that hosted Blackdome’s production runs right onto Discovery Energy Metals‘ JV ground. Historical placer production at Fairless Creek yielded 1,770 kilograms of gold (1931–1940) and recent rock sampling at the JV has returned up to 1.23 g/t gold (Borin Creek, sample 19BOR-2).32 Axiom Exploration’s 2021 airborne magnetic survey — 748 line-kilometres at 100 m line spacing — outlined the structural corridor the JV is now exploring.33 Recent studies have continued to demonstrate the importance of exploration around past producers and known vein systems, further increasing the probability that Discovery Energy Metals could be sitting on a meaningful discovery.

These examples highlight not only the proven mineral wealth of the regions Discovery Energy Metals (CSE: DEMC) has positioned in, but also the immense untapped potential that Discovery Energy Metals is poised to explore and could potentially develop in the coming months and years.34

The Right Copper Company At The Right Time

Recent disclosures from the company indicate that Discovery Energy Metals (CSE: DEMC) is advancing work on its portfolio across four distinct commodity targets aligned to the current supercycle and criticals-basket themes.35 This is a first step that could lead to further momentum as work programs are detailed and put into action by the company to advance each project.

Discovery Energy Metals (CSE: DEMC) is advancing with clear-cut strategies that are set to position the company as a leader in small-cap North American copper-and-criticals exploration, across a continent burgeoning with untapped mineral wealth. By focusing on multiple commodity classes simultaneously, Discovery is leveraging the full spectrum of its portfolio’s potential.

In recent disclosures published by Discovery Energy Metals (CSE: DEMC), several key initiatives are clear, including:

Copper + Molybdenum

A Focus on Copper Porphyry at Crystal Lake

The term “porphyry” refers to a style of copper deposit characterized by large-scale, low-to-moderate-grade mineralization, typically the foundation of the world’s biggest copper mines. Discovery’s flagship 5,283-hectare Crystal Lake Copper-Molybdenum Project in central British Columbia is an early-stage Cu-Mo porphyry property in a well-mineralized district, with year-round road access, a roughly 2.3-kilometre magnetic porphyry target already outlined, and grab samples up to 0.70% Cu (Raven at 7,577 ppm Cu) plus accompanying Ag and Au.36

The acquisition included a skin-in-the-game earn-in trigger: an additional $200,000 cash and 1,000,000 shares are due if the project delivers a drill intercept exceeding 0.5% copper over 100 metres, or an equivalent grade-thickness combination — call it the 0.5% × 100 m trigger.37 That is not the kind of milestone negotiated by a team planning to shuffle paper. It is what you write into a deal when you know what result would change the market’s mind.

Gold + Silver

Epithermal Gold-Silver At Koster Dam

With a goal to advance its epithermal gold-silver JV adjacent to a former-producing mine, Discovery holds a 45% interest in the Koster Dam Joint Venture — 9 claims totaling 4,535 hectares in south-central British Columbia, approximately 7 km north of and contiguous with the former-producing Blackdome gold-silver mine.39

- Cariboo Rose Resources holds the remaining 55% and is the initial managing operator.

- The technical content is authored by Geoffrey Goodall, P.Geo. (Global Geological Services Inc.), in the February 20, 2023 NI 43-101.

- Vein-hosted gold-silver, properly de-risked, represents a lucrative opportunity, promising higher yields as operations scale.

Copper + Gold

Carlin-Type Gold Exposure at ESN

ESN is a Carlin-type gold property.33 unpatented lode claims covering approximately 660 acres in White Pine County, Nevada.23

White Pine County also hosts KGHM’s producing Robinson copper-gold mine.24

More importantly, ESN sits within the belt that includes the Battle Mountain gold trend and the Bald Mountain gold mine — the asset Kinross paid US$610 million for in January 2016.25,38

This is not “an overlooked U.S. gold asset.”

It is a Carlin-type claim block along a trend where a single major operator has already written a nine-figure cheque for commodity-aligned exposure.

Technical content in the ESN NI 43-101 Technical Report (Effective Date March 1, 2022) was authored by Bradley C. Peek, MSc, CPG.

Lithium + Cesium + Tantalum

LCT-Pegmatite Criticals Exposure Across Québec

Discovery’s aggregate Québec land position spans over 225,000 hectares across James Bay, Nunavik and eastern Québec focused on lithium-cesium-tantalum (LCT) pegmatite systems — with a combined Canada-plus-Nevada total of approximately 235,000 hectares across its full portfolio.40

LCT pegmatites are the rock type that hosts most of the world’s hard-rock lithium production and an increasing share of tantalum — both on the U.S. Critical Minerals list.

An Ambitious, Forward-Looking Approach

The company’s strategic initiatives underscore its multifaceted approach to resource exploration, balancing immediate copper-porphyry work with parallel Carlin-type gold advance, epithermal JV progression and a continental-scale criticals land bank. In an era where copper continues to be a sought-after asset and critical minerals have never been more strategically valuable, the company’s methodical and phased strategy — beginning with the flagship Crystal Lake Cu-Mo porphyry target41 and layering gold and criticals exposure alongside — positions Discovery Energy Metals (CSE: DEMC) for success in the competitive landscape of small-cap North American mineral exploration.

With a strategic foothold in multiple productive mining districts, Discovery Energy Metals (CSE: DEMC)‘s actions towards operationalizing its assets reflect a clear trajectory towards becoming a pivotal player in the copper-and-criticals sector.

Rare Opportunity Before the Crowd

When investing in copper juniors, timing is everything. That’s why Discovery Energy Metals (CSE: DEMC) represents a rare opportunity for investors to own a company in the right area at the early stages, before any major developments that could cause the valuation to skyrocket.

Everyone knows it’s the early bird that gets the worm and right now, our readers have the opportunity to delve into Discovery Energy Metals (CSE: DEMC) before the rest of the market learns about this growing story. Sometimes the most important thing in investing is not necessarily being right all the time, but rather, investing early when you are.

The Lithium Factor:

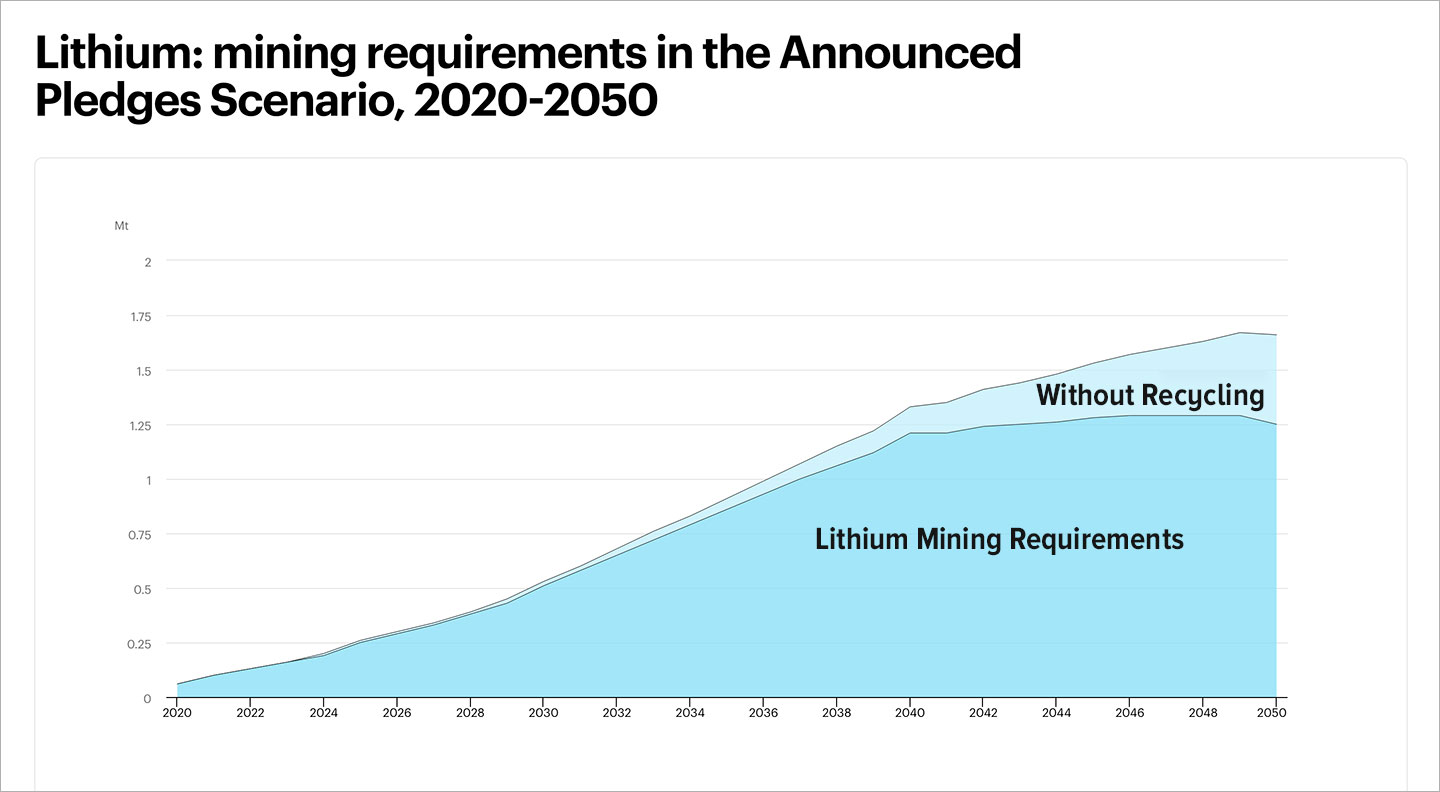

Copper is only the first of the three supercycles now stacking on Discovery Energy Metals (CSE: DEMC)‘s share structure. The second is lithium — and it was just confirmed by one of Canada’s most respected sell-side research desks on the very day this article was finalized.

On April 22, 2026, Canaccord Genuity published a research note calling the lithium market into a material deficit beginning in 2026 and extending through 2035, with the expected 2027–2028 price rises described as insufficient to close the structural supply gap absent further disruption.65

That is not a cautious “we might get tight” whisper from a mid-tier broker. That is one of the top capital-markets names in Canadian resource research calling a structural deficit for nine consecutive years on a commodity already sitting on the U.S. 2025 Critical Minerals list.67

Layer the Canaccord call onto the fact that lithium, tantalum, and cesium are all three on the U.S. 2025 Critical Minerals list alongside copper,67 and the picture sharpens fast. A junior that holds ground capable of working multiple criticals at once is no longer a “criticals tag” in the marketing deck. It is an infrastructure-scale option on an EV-plus-A.I.-plus-electrification demand curve that is going near-vertical at the same moment the supply pipeline is structurally short. The U.S. and Canadian federal criticals frameworks were not written to politely acknowledge commodities that happen to be useful. They were written to fast-track Western-aligned production of commodities the policy apparatus has already identified as strategic single-points-of-failure.

Here is where that lands for Discovery Energy Metals (CSE: DEMC). The rock that hosts most of the world’s hard-rock lithium — and an increasing share of its tantalum and cesium — is the LCT-pegmatite system (lithium-cesium-tantalum). Québec is one of the world’s premier LCT-pegmatite jurisdictions. Discovery Energy Metals holds over 225,000 hectares across Québec specifically targeting LCT-pegmatite systems,40 spanning James Bay, Nunavik, and eastern Québec — aggregating to roughly 235,000 hectares across its full Canada-plus-Nevada portfolio. That is not a token criticals bullet. That is a continental-scale land bank on the rock type Canaccord just called a nine-year structural-deficit curve — held inside a CSE-listed vehicle with a market capitalization of approximately $15.34 million on the April 14, 2026 close.23

- One sub-$16-million-market-capitalization issuer.

- Three criticals (lithium, cesium, tantalum) on the U.S. 2025 list.

- A nine-year Canaccord-called deficit window on the lead commodity.

- A 225,000-hectare Québec land bank on the rock type the deficit is measured against.

The Gold Factor:

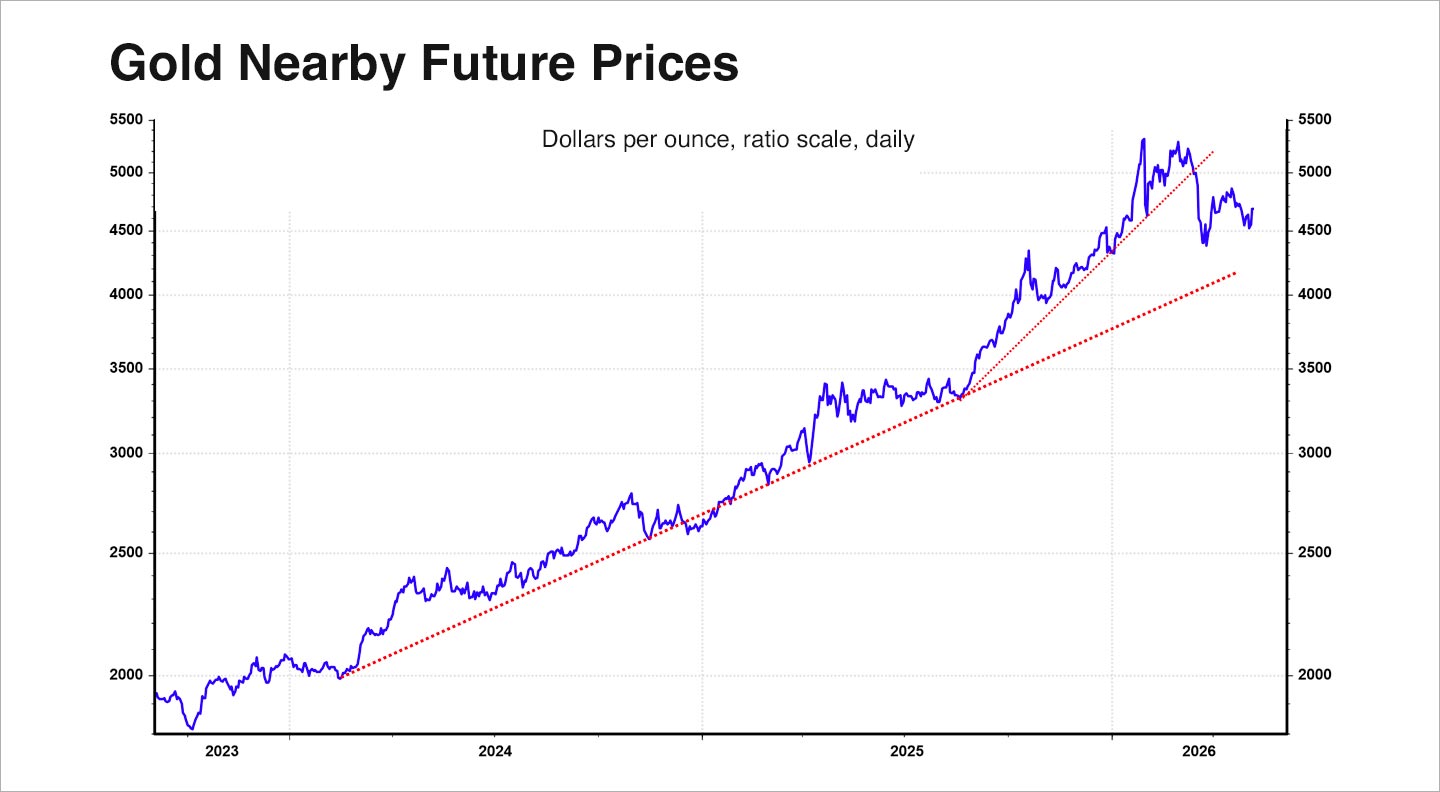

Gold futures have already crossed above US$5,000 per ounce multiple times in 2026,66 validating the bold call we published while everyone else was still defending a ~US$3,500/oz projection for the year.

Central-bank buying, de-dollarization flows, Western-supply fragility, and the loss of confidence in fiscal arithmetic across multiple sovereign balance sheets are the forces behind it, and they are not going away.

That matters specifically for Discovery Energy Metals (CSE: DEMC) because the company is not retrofitting a gold narrative onto a copper story. The gold exposure was already there, at corporate inception, on two already-defined legs sitting on the same share structure that carries Crystal Lake and the Québec LCT-pegmatite land bank:

The Bald Mountain Adjacency (ESN Project, Nevada). The ESN Project sits along the same belt that hosts Kinross Gold’s Bald Mountain gold mine, a Carlin-type system Kinross acquired from Barrick Gold for US$610 million in January 2016.26 That is a nine-figure senior-producer cheque written for commodity-aligned exposure in the very same belt Discovery Energy Metals (CSE: DEMC) is claiming. The ESN Project consists of 33 unpatented lode claims covering approximately 660 acres in White Pine County, targeting Carlin-type gold mineralization.27 This is not “an overlooked U.S. gold stub.” It is a Carlin-type gold claim block along a trend where a major operator has already proven the capital willingness by writing a nine-figure cheque for the adjacent ground.

The Blackdome Shadow (Koster Dam JV, British Columbia). The Koster Dam Joint Venture — 9 claims totaling 4,535 hectares, held 45% by Discovery Energy Metals (CSE: DEMC) with Cariboo Rose Resources as managing operator — sits contiguous with and approximately 7 kilometres north of the former-producing Blackdome gold-silver mine.31 This is not a greenfield guess. Historical placer production at Fairless Creek yielded 1,770 kilograms of gold (1931–1940), and recent rock sampling at the JV has returned up to 1.23 g/t gold (Borin Creek, sample 19BOR-2).32 Axiom Exploration’s 2021 airborne magnetic survey — 748 line-kilometres at 100 m line spacing — outlined the structural corridor the JV is now exploring.33 Two producing or formerly-producing gold mines hosted this same corridor. Discovery Energy Metals sits on it.

Two gold legs. One on a belt a major is already spending hundreds of millions of dollars on. One on a corridor a past producer has already mined. Paired onto a share structure that is simultaneously carrying Crystal Lake’s Cu-Mo porphyry target in British Columbia and Québec’s 225,000-hectare LCT-pegmatite land bank. That is the clean three-supercycle thesis spelled out: copper structurally short with Reuters’ highest-ever 2026 analyst consensus,5 lithium called into a nine-year Canaccord-flagged deficit65 on a 225,000-hectare LCT-pegmatite footprint,40 and gold already trading above US$5,000 per ounce on live tape66 with two already-positioned gold legs on the same CSE-listed vehicle carrying a market capitalization of approximately $15.34 million.23

Three supercycles. One ticker. One share structure. That is what we mean by Stacking Supercycles.64

A Long History Of Major Wins & Exploration Track Record

Of ultimate importance in any industry and of particular importance in the mining space is the experience and credentials of the team leading the exploration efforts. In the case of Discovery Energy Metals (CSE: DEMC), there’s no shortage of experienced executives with a long history of leading multiple developing companies in the resource sector, followed by multi-bagger returns, takeouts and top-tier investor outcomes.42

If there’s any team that knows first-hand the conditions necessary to drive a successful junior resource company, it’s this team right here:

Mr. Mike Hodge came up through the field, beginning his exploration career on the original staking program for the Blue River tantalum-niobium project in 1999, and has since worked on more than 25 exploration projects across North America.43 That gives him ground-floor exploration experience most small-cap executives do not have. His background also includes years of capital-raising and deep participation in the resource-conference circuit, which means he understands both sides of the junior mining equation — the rocks and the market.

Mr. Eric Negraeff brings over 20 years of capital-markets experience — currently Vice President of Corporate Development at Incite Capital Markets, and previously with PI Financial and C.M. Oliver.44 He has also built and managed a profitable proprietary-trading division and spent years raising capital for small- and mid-cap companies. Junior mining stories do not re-rate on geology alone. They re-rate when the company can finance, position, and stay in front of the right audience. Negraeff gives Discovery Energy Metals (CSE: DEMC) real strength on that front.

Mr. Nate Schmidt brings more than 12 years of exploration experience, including planning and managing multi-drill and ground programs, building geological models, and working directly with porphyry Cu-Mo systems — the geological setting Discovery Energy Metals (CSE: DEMC) is targeting at Crystal Lake.45 Outside Discovery Energy Metals, he serves as Canada West & Territories Operations Director at Dahrouge Geological, where his profile is tied to 110-plus projects. For a copper porphyry story, he may be the single most directly relevant geologist on the board.

Ms. Jody Bellefleur gives Discovery Energy Metals (CSE: DEMC) something every serious junior needs: a finance executive with long experience in the public resource markets who has already been attached to a major run. She has more than 25 years of corporate accounting experience and concurrently serves as Chief Financial Officer of Q2 Metals Corp. (TSXV: QTWO).46 Q2’s share price rose +214% in 2024; its market capitalization grew +380% in the same year; and it ranked 9th on the 2025 TSX Venture 50, representing a real-world public-markets win Bellefleur was in the CFO seat to watch unfold.47 As of April 2026, Q2 carried a market capitalization in the $483M–$567M range.48 Discovery is not Q2. That is not the claim. The claim is that Discovery shares a senior financial executive with a company that the Venture market has already ranked among its top-10 performers of the prior year. That is not a coincidence you ignore.

Mr. Colton Griffith adds another piece many technically oriented juniors lack: the ability to shape the story for the market. His background is in corporate positioning, investor communications, and capital-markets strategy for public resource companies across North America, including work with Zimtu Capital Corp.’s ADVANTAGE program.49 Good stories do not automatically get noticed. They need to be framed properly, communicated properly, and put in front of the right investors at the right time. Griffith adds that layer.

Mr. Nicholas Rodway (EGBC #46541) is the independent Qualified Person as defined by National Instrument 43-101 — Standards of Disclosure for Mineral Projects, who reviewed and approved the technical content relating to the Crystal Lake Copper Property.50

Mr. Geoffrey Goodall (Global Geological Services Inc.) is the author of the Koster Dam NI 43-101 Technical Report dated February 20, 2023, and the Qualified Person for technical content relating to the Koster Dam Joint Venture.51

Mr. Bradley C. Peek is the author of the ESN NI 43-101 Technical Report dated March 1, 2022, and the Qualified Person for technical content relating to the ESN Project in White Pine County, Nevada.52

With such an extensive history of exploration experience, capital-markets reach, porphyry Cu-Mo expertise, and direct connectivity to one of the recent top-10 TSX Venture performers, this team promises a bright future for Discovery Energy Metals (CSE: DEMC) and its stakeholders.

Insider Alignment

When assessing the quality of any potential investment, it’s important to consider if management’s incentives are aligned with shareholders. Is it any surprise then, given the high-potential situation here, that the management team of Discovery Energy Metals (CSE: DEMC) holds notable equity positions disclosed in regulatory filings? This information is available on SEDI (System for Electronic Disclosure by Insiders) and SEDAR+,53 confirming a key sign of alignment of incentives with shareholders. It demonstrates the dedication that these executives have to the long-term success of the company.

The Big Potential Winner In The Copper Supercycle

If history is any indication, it’s the smaller mining companies that position themselves for significant upcoming milestones that deliver out-sized returns for investors. That’s why we believe Discovery Energy Metals (CSE: DEMC) is the one company you must start to closely follow right away.

Based on everything uncovered during the course of our reporting, Discovery Energy Metals (CSE: DEMC) stands on the cusp of unlocking significant value for its stakeholders and presents itself as an urgent and pressing matter for any serious investor to research as quickly as possible.

The situation in copper is hard to ignore, and with more and more major-company capital being deployed into the sector with each growing week, it seems only a matter of time until the next major development comes bursting out of the junior copper space.

Serious investors would do well to add Discovery Energy Metals (CSE: DEMC) to the top of their watch-list for the remainder of 2026. You don’t want to regret missing this one, so prioritize your due diligence and don’t delay your research on this investment.

10 Key Reasons To Prioritize Discovery Energy Metals (CSE: DEMC) in 2026

In the dynamic and ever-evolving copper and critical-minerals sector, identifying companies with strong growth potential, strategic positioning, and robust operational foundations is crucial for investors seeking to maximize their returns. Discovery Energy Metals (CSE: DEMC), with its strategic initiatives and market positioning, stands out as a compelling investment opportunity for 2026.

Below, we delineate the key factors that underscore Discovery Energy Metals (CSE: DEMC)‘s potential to outperform within the copper-and-criticals sector, offering investors a clear framework for evaluating its prospects.

With such a strong combination of factors, Discovery Energy Metals (CSE: DEMC) presents a compelling case for consideration by investors looking to capitalize on the opportunities within the copper-and-criticals sector in 2026. Its strategic assets, capable leadership team, and clear vision for growth make Discovery Energy Metals poised to deliver significant value to its shareholders in the coming copper supercycle.

Ask Yourself One Question

Before you decide what to do with Discovery Energy Metals (CSE: DEMC), go back to Foran Mining in April 2020. Ten cents per unit on a non-brokered placement. No one was paying attention!11

Six years later, Eldorado Gold paid approximately $6.25 per Foran share to take the company out — a 62.5× per-share outcome, a +6,150% return on that April 2020 placement, closed on April 14, 2026.12

Think to yourself, if you could’ve bought Foran at 10 cents before it ran to $6, how much would you have bought?

You may have a rare second chance here with Discovery Energy Metals (CSE: DEMC).

Further Research and Reading:

For professional investors seeking to validate these insights and conduct a deeper evaluation of Discovery Energy Metals (CSE: DEMC) within the context of the 2026 copper-and-criticals landscape, a comprehensive list of sources and recommended readings is provided below. These references offer a wealth of data, analyses, and expert opinions essential for a well-rounded investment decision-making process.

- Reuters: January 2026 Analyst Copper Poll

- Canadian Securities Exchange (CSE): Discovery Energy Metals (CSE: DEMC) Listings and Filings

- Mining.com: Bloomberg Intelligence — Copper Share of 2026 Diversified-Miner EBITDA

- Kitco News: Copper Price Coverage

- International Copper Study Group: 2026 Copper Market Forecast

This curated selection of resources is designed to provide investors with a comprehensive foundation for their research on Discovery Energy Metals (CSE: DEMC) and the broader investment landscape in the copper-and-criticals sector for 2026.

Sector: Copper / Critical Metals / Gold Exploration

1https://metalcharts.org/copper-all-time-high , Reuters — January 2026 analyst copper poll: 2026 average US$11,975/mt, the highest annual consensus Reuters has ever recorded.

2 International Energy Agency — Critical Minerals Outlook: copper approximately 30% supply gap by 2035 between announced projects and projected demand. International Copper Study Group — 2026 forecast 150,000-tonne refined copper market deficit.

3 Capital Rankings track-record reference articles: prior featured issuers TMAS (engaged at $2.34 split-adjusted, high $20.43 split-adjusted, +772%) and ELEM (engaged at $6.70 split-adjusted, high $16.50 split-adjusted, +145%). See Capital Rankings track-record disclosures and prior coverage archive.

4 Discovery Energy Metals Corp. — CSE listing page.

5https://news.metal.com/es/newscontent/103781916-UBS-Sharply-Raises-Copper-Price-Forecast-Sees-Prices-Hitting-15000 , Reuters — January 2026 analyst copper poll: 2026 average US$11,975/mt.

6https://news.metal.com/es/newscontent/103781916-UBS-Sharply-Raises-Copper-Price-Forecast-Sees-Prices-Hitting-15000 , J.P. Morgan Commodities Research — 2026 copper forecast approximately US$12,075/mt average, Q2 2026 peak US$12,500/mt.

7https://investinglive.com/commodities/copper-refuses-to-break-despite-the-iran-war-20260511/ , Citi Commodities Research — 2026 copper base case US$10,500/mt average; bullish scenario path to US$13,000–US$15,000/mt.

8https://www.ft.com/content/725234a6-9e6f-4a4a-9406-2bda667ca511 , Bank of America Global Research — 2026 copper forecast approximately US$11,313/mt. Goldman Sachs Commodities Research — 2026 copper forecast range US$10,000–US$11,000/mt.

9 Bloomberg Intelligence via Mining.com — copper projected to account for more than 35% of diversified miners’ 2026 EBITDA.

10 Foran Mining Corp. — “Foran Non-Brokered Private Placement Closes, Over-subscribed by $210,000,” April 29, 2020; $2 million closed at $0.10 per unit.

11 Eldorado Gold Corporation — “Eldorado and Foran Combine to Create a Leading Gold and Copper Producer,” February 2, 2026; consideration 0.1128 Eldorado shares plus US$0.01 cash per Foran share, approximately $6.25 per Foran share at announcement.

12 Derived calculation: $6.25 ÷ $0.10 − 1 = 62.5× = +6,150%. Inputs per footnotes 10 and 11.

13 Derived calculation: $10,000 × 62.5 = $625,000. Inputs per footnote 12.

14 S&P Global Market Intelligence / industry aggregated data — copper head grades declined approximately 40% since 1991.

15 S&P Global Market Intelligence — “World Exploration Trends” report: 14 of 239 copper deposits brought into development since 2013 qualify as genuine new discoveries.

16 International Energy Agency — “The Role of Critical Minerals in Clean Energy Transitions”: new copper mine development timelines can stretch up to 25 years from discovery to first production.

17 United States Geological Survey — “U.S. Geological Survey Releases 2025 List of Critical Minerals” (copper added).

18 International Energy Agency — Critical Minerals Outlook.

19 International Copper Study Group — 2026 forecast 150,000-tonne refined copper market deficit.

20 International Copper Study Group / IEA aggregated data — global copper mine production 22.8 Mt in 2024; projected decline below 19 Mt by 2035 on current project pipelines.

21 Eldorado Gold Corporation — “Eldorado Gold Completes Acquisition of Foran Mining,” April 14, 2026; transaction value approximately $3.8 billion.

22 Hudbay Minerals Inc. — “Hudbay Announces Agreement to Acquire Arizona Sonoran Copper Company for $1.48 Billion.”

23 CSE historical OHLC for DEMC — April 14, 2026 close $0.20. Shares outstanding 76,686,654 per MD&A for the nine months ended October 31, 2025. Market-cap calculation: $0.20 × 76,686,654 = $15,337,331 (~$15.34M).

24 Discovery Energy Metals Corp. — MD&A for the nine months ended October 31, 2025 (shares outstanding 76,686,654).

25 Discovery Energy Metals Corp. — 2026 Corporate Presentation.

26 Kinross Gold Corporation — “Kinross Agrees to Acquire Bald Mountain Mine and 50% of Round Mountain Mine from Barrick for Total Consideration of US$610 Million,” January 11, 2016.

27 Discovery Energy Metals Corp. — ESN Project NI 43-101 Technical Report, Effective Date March 1, 2022, QP Bradley C. Peek, MSc, CPG; 33 unpatented lode claims covering approximately 660 acres in White Pine County, Nevada.

28 Discovery Energy Metals Corp. — “Discovery Energy Metals to Acquire 100% of Crystal Lake Copper Property in British Columbia,” June 17, 2025; 5,283 hectares / 8 contiguous claims / ~34 km south of Fort Fraser, BC.

29 Discovery Energy Metals Corp. — Crystal Lake PR (June 17, 2025): grab samples up to 0.70% Cu with the Raven Showing at 7,577 ppm Cu (~0.76%); accompanying silver and gold values. Technical source: Entrée Gold 2010 Prospecting, Geochemical, Geophysical Report, ARIS #31727.

30 Discovery Energy Metals Corp. — Crystal Lake PR (June 17, 2025): approximately 2.3-kilometre magnetic porphyry target; copper-bearing diorite porphyry stockwork running north-south from Holler Lake to Bennett Lake.

31 Discovery Energy Metals Corp. — Koster Dam NI 43-101 Technical Report, Effective Date February 20, 2023, QP Geoffrey Goodall, P.Geo. (Global Geological Services Inc.); 9 claims totaling 4,535 hectares in south-central BC; 45% joint-venture interest; property approximately 7 km north of and contiguous with the former-producing Blackdome gold-silver mine.

32 Koster Dam NI 43-101 (February 20, 2023) — historical placer production at Fairless Creek (1,770 kg gold, 1931–1940); 2019 rock sample 19BOR-2 returning 1.23 g/t Au at Borin Creek; 2018 stream-sediment sampling maximum 3,750 ppb Au.

33 Koster Dam NI 43-101 (February 20, 2023) — Axiom Exploration 2021 airborne triaxial magnetic survey, 748 line-kilometres at 100 m line spacing.

34 Discovery Energy Metals Corp. — 2026 Corporate Presentation.

35 Discovery Energy Metals Corp. — press releases and 2026 Corporate Presentation.

36 Discovery Energy Metals Corp. — Crystal Lake acquisition PR (June 17, 2025) and Crystal Lake project page.

37 Discovery Energy Metals Corp. — Crystal Lake PR (June 17, 2025), Acquisition Terms — Bonus Consideration: additional $200,000 cash and 1,000,000 common shares payable on drill intercept exceeding 0.5% Cu over 100 metres (or equivalent grade/interval).

38 Discovery Energy Metals Corp. — ESN Project NI 43-101 Technical Report (March 1, 2022, QP Bradley C. Peek, MSc, CPG). Kinross Gold Corporation — Bald Mountain / Round Mountain acquisition PR, January 11, 2016.

39 Discovery Energy Metals Corp. — Koster Dam NI 43-101 (February 20, 2023) and project page.

40 Discovery Energy Metals Corp. — 2026 Corporate Presentation: over 225,000 hectares across Québec (James Bay, Nunavik, eastern Québec) focused on LCT-pegmatite systems; aggregate ~235,000 hectares across Canada and Nevada.

41 Discovery Energy Metals Corp. — Crystal Lake project page and Crystal Lake PR (June 17, 2025).

42 Discovery Energy Metals Corp. — Management & Directors page.

43 Discovery Energy Metals Corp. — Mike Hodge biography (Blue River tantalum-niobium staking 1999; 25+ exploration projects across North America).

44 Discovery Energy Metals Corp. — Eric Negraeff biography (VP Corporate Development at Incite Capital Markets; prior PI Financial and C.M. Oliver; 20+ years of capital-markets experience).

45 Discovery Energy Metals Corp. — Nate Schmidt biography (12+ years exploration experience; porphyry Cu-Mo systems; Canada West & Territories Operations Director at Dahrouge Geological, 110+ projects).

46 Discovery Energy Metals Corp. — Jody Bellefleur biography (25+ years corporate accounting experience; concurrent CFO of Q2 Metals Corp.).

47 Q2 Metals Corp. — issuer communications and TSX Venture 50 disclosures; 2024 share-price appreciation +214%; market-cap growth +380%; ranked 9th on the 2025 TSX Venture 50.

48 Q2 Metals Corp. — April 2026 trading data (market capitalization range $483M–$567M across trailing trading period surveyed).

49 Discovery Energy Metals Corp. — Colton Griffith biography (Marketing Manager, Zimtu Capital Corp.; capital-markets strategy; Zimtu ADVANTAGE program).

50 Nicholas Rodway, P.Geo. (EGBC #46541) — QP for Crystal Lake technical content. Discovery Energy Metals Corp. issuer disclosures.

51 Geoffrey Goodall, P.Geo. (Global Geological Services Inc.) — author of the Koster Dam NI 43-101 Technical Report dated February 20, 2023.

52 Bradley C. Peek, MSc, CPG — author of the ESN NI 43-101 Technical Report dated March 1, 2022.

53 Canadian Securities Administrators — SEDI (System for Electronic Disclosure by Insiders).

54 Reuters — January 2026 analyst copper poll. J.P. Morgan Commodities Research. Citi Commodities Research.

55 United States Geological Survey — 2025 List of Critical Minerals.

56 Discovery Energy Metals Corp. — Crystal Lake project page and Crystal Lake acquisition PR (June 17, 2025).

57 Discovery Energy Metals Corp. — Crystal Lake PR (June 17, 2025), Acquisition Terms — Bonus Consideration.

58 Kinross Gold Corporation — Bald Mountain / Round Mountain acquisition PR, January 11, 2016.

59 Discovery Energy Metals Corp. — Koster Dam NI 43-101 (February 20, 2023) and project page.

60 Discovery Energy Metals Corp. — 2026 Corporate Presentation (Québec LCT-pegmatite land position). United States Geological Survey 2025 Critical Minerals List. Natural Resources Canada critical-minerals strategy.

61 Q2 Metals Corp. — TSX Venture 50 ranking (#9 on 2025 list); +214% 2024 share-price appreciation; +380% 2024 market-cap growth.

62 Discovery Energy Metals Corp. — Nate Schmidt biography. Dahrouge Geological.

63 Eldorado Gold Corporation — “Eldorado Gold Completes Acquisition of Foran Mining,” April 14, 2026. CSE historical OHLC for DEMC.

64 “Stacking Supercycles” — Capital Rankings proprietary thesis synthesizing the compounding of simultaneous structural shortages across copper (footnotes 1–2, 17–20), lithium (footnotes 65 & 67), and gold (footnote 66) on a single issuer’s share structure. (author commentary).

65 Canaccord Genuity via Mining.com — “Lithium market to enter deficit until 2035, says Canaccord,” April 22, 2026. Material lithium deficit beginning in 2026 and extending through 2035, with the expected 2027–2028 price rises described as insufficient to close the structural supply gap absent further disruption.

66 Gold futures live tape — US$5,000+/oz printed multiple times in 2026, validating the Capital Rankings US$5,000+/oz call made when the consensus was still defending ~US$3,500/oz for 2026.

67 United States Geological Survey — “U.S. Geological Survey Releases 2025 List of Critical Minerals” (lithium, tantalum, cesium, copper all on the 2025 list).

68 Behavioral-finance and position-sizing bibliography: Kahneman & Tversky, “Prospect Theory: An Analysis of Decision under Risk” (Econometrica, 1979); Tversky & Kahneman, “Advances in Prospect Theory” (Journal of Risk and Uncertainty, 1992); Kahneman, Thinking, Fast and Slow (2011); Jeff Bezos regret-minimization framework (Amazon founder letters, 1997 onward); Nassim Nicholas Taleb, Antifragile: Things That Gain from Disorder (Random House, 2012) — barbell strategy; Howard Marks, The Most Important Thing (Columbia Business School Publishing, 2011) — “prepare, don’t predict”; J.L. Kelly, “A New Interpretation of Information Rate” (Bell System Technical Journal, 1956) — Kelly Criterion for bet sizing under uncertainty.

All information current of the article publication date of May 27th, 2026

This article is for speculative investors who are familiar with this type of investing. If you are not a speculative investor, please take time to read these important contextual notices as they contain explicit explanations of information that is expected to already be implicitly understood by our targeted and intended audience. Implicit assumptions about speculative investors include, but are not limited to, the following implied knowledge:

(i) HIGH RISK: Speculative investing involves an extremely high degree of risk by design. Speculative investing most often involves purchasing common equity in highly speculative companies (stock of issuers) that, if ultimately successful, will return extremely high rates of return to speculative investors who purchased shares early on. However, these high rates of return when a stock is successful are almost always offset (to varying degrees) by a much larger number of total failures that result in a near or actual total loss of capital invested. It is the object and purpose of speculative investing to have the few winners return so great of returns that they pay for all your investment losses with extra profit leftover, however, this is not always the case and sometimes speculative investing can result in the returns obtained from winners not exceeding the losses generated by losers. Timing also plays a large role. Investors who purchase earlier are often in a position to make higher overall profits and investors who sell near the highs, or who can cut their losers quickly and reduce the losses on losers, are often better able to manage a higher ratio of dollars won vs. dollars lost. As with anything, speculative investing involves a considerable number of factors that are often unpredictable. IT IS POSSIBLE TO LOSE YOUR ENTIRE INVESTMENT WHEN ENGAGING IN SPECULATIVE INVESTING, EVEN WHEN PURCHASING A PORTFOLIO OF WELL-DIVERSIFIED SPECULATIVE TRADES.

(ii) SPONSORED ARTICLES: Speculative investors are aware and indeed look forward to (as they benefit from) the fact that issuers, including the issuer profiled in this article, regularly engage public awareness campaigns where they compensate publishers of information to distribute positive information about their company, highlighting the extreme bull case available if their company succeeds. These campaigns are intended and often do attract a large amount of investors to pay attention to the company, highlighting the speculative value of the shares, which can result in tremendous momentum runs being sparked in the company’s shares and can often result in wild swings in the stock price, generating large returns for early investors but can also have the effect of generating large losses for purchasers who buy near the highs as a reality of how stock trading trends generally work. No one has a crystal ball and no one can predict whether a certain stock will go up, down, sideways with absolute certainty, even during an awareness campaign as the ultimate arbiter of value is the actual market itself and sometimes the market decides a company’s value is worth less after the campaign than before. Our audience understands that we are paid in connection with this campaign. A full disclosure of this contract is available in the “Public Awareness Campaign” section below.

(iii) FOCUS ON SPECULATIVE INFORMATION: Speculative investors understand that these articles focus more on ongoing momentum and performance than a traditional “value investing” approach would, as this is a 200-year-old proven strategy in the stock market (CFA Institute: https://rpc.cfainstitute.org/en/research/financial-analysts-journal/2016/how-durable-is-momentum-investing). Often these companies are early-stage and do not have much to speak of in terms of a value-investing analysis, and so price performance, momentum and speculative-investing terminology are the most appropriate way for speculative investors to read about the company. This results in the article highlighting the potential bull-case performance, because the high risks of total loss are already known to this audience of speculative investors; it is not novel to feature. The new and novel information is the specific upside and bull case regarding the specific issuer, and that is why that information is featured prominently and other information is omitted or not featured as prominently. This has to do with the audience and their expectations, desires, and needs.

(iv) TRACK RECORD INFORMATION: Speculative investors further understand that highlighted past performance is talking about the lowest starting price and the highest trading price achieved since the publication of our article, and it is not expected nor practical for us to continue following the company after the catalysts have potentially occurred and the contract period is up. Further, speculative investors are aware that trade-record information does not purport to be a complete record of every article we have published and no speculative investor expects this to be the case. It is industry standard in the world of speculative investing that we might only have 1 winner in a basket of losers, and that is what our audience is looking to read about and understand it is reading about the highlights of the past and that the others are potentially total losses.

(v) TARGETING OF TRAFFIC: Speculative investors understand that we pay to place this article using a variety of methods including sponsored posts, native ads, search ads, and display ads in a manner designed to target solely speculative investors who have expressed interest in other content, terms, or patterns that would indicate they engage in or wish to engage in speculative investing. We do not purposefully target an audience that is looking for risk-free returns or safe government bonds or other guaranteed investment instruments, and in fact such targeting would cost us money and decrease our effectiveness for our clients. In the event that you believe you have been incorrectly targeted, please contact us on our contact form and provide as much detail as possible as to why you believe you may have been incorrectly categorized as a speculative investor.

(vi) FOCUS ON BEST CASE SCENARIOS: Speculative investors prefer to read articles that get straight to the point in the title BECAUSE THIS IS A TIME-SAVING HEURISTIC DEPLOYED BY SUCCESSFUL SPECULATIVE INVESTORS, highlighting the best case scenario upfront including, preferably, the percentage by which an issuer could rise. Speculative investors are well-versed and experienced enough to understand that this does not guarantee that these results will be achieved or are even the most likely or even probable scenario. All that is expected is that we hold a bona fide belief in the possibility that such a scenario could be achieved, even if unlikely, since that is the point of speculative investing (to find situations that could return hundreds of percentage gains and bring them to the speculative investors’ attention for their own judgment and consideration for their speculative portfolio). Speculative investors also prefer that we do not waste precious time and space within an article talking about risks as these are well-known and, practically, the same (total risk of loss, regardless of the specifics that may cause it).

To reiterate, this article was written for speculative investors who are looking to read a niche article that highlights tremendous upside that could result from speculative investments and who understand that this does not mean it is the most likely outcome, and further expect and understand that we are paid to do this (fully disclosed below). If you are not in this audience, please note that this article is not meant for you to read. We encourage you to read the disclaimers and disclosures below and decide for yourself if you wish to continue reading our articles.

(The below is not an exhaustive list or analysis.)

1. For the last few stocks we wrote about that saw impressive gains, please refer to the announcements where we were engaged by TMAS at $2.34 per share (split adjusted) and it ran to over $20.43 per share at the high (split-adjusted) and where we were engaged by ELEM at $6.70 per share (split adjusted) and it ran to $16.50 at the high (split-adjusted). Those results exceed +772% gains and +145% gains respectively. It is of material importance to our audience that we discuss our past performance as, even though it may not be indicative of future performance, it is of interest to the average reader in our audience. It is a heuristic commonly deployed by speculative investors who have limited time and attention to decide what articles to give attention to and what to further investigate. Failure to do so would be a disservice to our audience and disrespect their time and intelligence.

2. The +6,150% per-share figure cited in this article is a historical calculation describing an actual Foran Mining shareholder’s return (April 2020 placement price $0.10 → February 2026 Eldorado Gold deal consideration of approximately $6.25 per Foran share, closing April 14, 2026). The derivation is arithmetic: $6.25 ÷ $0.10 − 1 = 62.5× = +6,150%. This is a historical, issuer-specific Foran figure — it is expressly not a forecast, guarantee, representation or promise of any kind that Discovery Energy Metals Corp. (CSE: DEMC) will achieve a comparable per-share outcome. Junior-mining per-share returns at any issuer are further modulated by dilution, execution risk, exploration outcomes, permitting, financing, and market conditions.

3. For copper market information and projections, much of this information was obtained from the January 2026 Reuters analyst poll (https://www.reuters.com/markets/commodities/), J.P. Morgan Commodities Research (https://www.jpmorgan.com/insights/research/copper-prices), Bank of America Global Research, Goldman Sachs Commodities Research, Citi Commodities Research (publicly disseminated in early 2026), and Bloomberg Intelligence as reported by Mining.com (https://www.mining.com/). Supply-demand framing is additionally drawn from the International Energy Agency (https://www.iea.org/reports/critical-minerals-outlook), the International Copper Study Group (https://icsg.org/), the United States Geological Survey (https://www.usgs.gov/), and S&P Global Market Intelligence.

4. Information about Discovery Energy Metals Corp. and its projects was obtained from the Company’s website (https://discoveryenergymetals.com/), its press releases (https://discoveryenergymetals.com/news/), its SEDAR+ disclosure record (https://www.sedarplus.ca/), its CSE listing page (https://thecse.com/listings/discovery-energy-metals-corp/), its 2026 Corporate Presentation, its MD&A for the nine months ended October 31, 2025, and the NI 43-101 Technical Reports for its Crystal Lake, Koster Dam, and ESN Project properties. Primary issuer and technical-report sources take priority over any third-party summary.

5. Comparable M&A transactions referenced (BHP/Oz Minerals, BHP-Lundin/Filo Corp, Hudbay/Arizona Sonoran, South32/Arizona Mining, Glencore/Teck Coal, Anglo American/Teck Resources, and most saliently Eldorado Gold/Foran Mining) are cited from the respective acquirer and target issuer press releases (linked in the Article Sources section above). These are real historical transactions cited to contextualize the pattern of copper-sector M&A activity; they are not a forecast that any comparable outcome will occur at Discovery Energy Metals Corp.

6. Further, the reason we focus so heavily and prominently on price performance is that there is over 200 years of evidence that momentum investing is one of the most robust and reliable strategies to generate excess returns (CFA Institute: https://rpc.cfainstitute.org/en/research/financial-analysts-journal/2016/how-durable-is-momentum-investing) and further, small-cap stocks tend to exhibit a stronger momentum effect and momentum generally provides higher risk-adjusted returns (Morningstar: https://www.morningstar.com/articles/591675/does-momentum-investing-work). As the CFA Institute notes, “the speculator is looking for hidden weak spots in the market,” and as such acts as “the advance agent of the investor, seeking always to bring market prices into line with investment values” (CFA Institute: https://blogs.cfainstitute.org/investor/2013/02/27/what-is-the-difference-between-investing-and-speculation-2/).

Risk Disclosures: Investing in mineral-exploration companies like Discovery Energy Metals Corp. (CSE: DEMC) involves substantial risks. There is no guarantee Discovery Energy Metals will make any discoveries or that its projects will enter production. Exploration efforts may be unsuccessful due to factors like lack of mineralization, challenging mining conditions, permitting issues, or financing difficulties. It is possible for investors to lose their entire investment in Discovery Energy Metals. Mineral exploration is inherently risky and speculative. Investors must be able to bear the risk of total loss.

Additional Project & Development Risk Factors: Mineral exploration and development are highly speculative and characterized by significant inherent risks that may result in the inability to successfully develop projects for commercial, technical, political, regulatory or financial reasons; even if successfully developed, projects may not remain economically viable for their mine life. Discovery Energy Metals Corp.’s (the “Company’s”) ability to identify mineral resources in sufficient quantity and quality, and to commence and/or complete development work and/or sustain commercial production, depends on numerous factors — many of which are beyond the Company’s control — including exploration success, the obtaining of funding for all phases of exploration, development and commercial mining, the adequacy of infrastructure, geological and metallurgical characteristics of any deposit, the availability of processing technology and capacity, the availability of storage capacity, the supply of and demand for critical and other minerals, the availability of equipment and facilities necessary to commence and complete development, the cost of consumables and mining and processing equipment, technological and engineering problems, accidents or acts of sabotage or terrorism, civil unrest and protests, currency fluctuations, changes in regulations, the availability of water, the availability and productivity of skilled labour, the receipt of necessary consents, permits and licenses (including mining licenses), and political factors, including unexpected changes in governments or governmental policies toward exploration, development and commercial mining activities. Cost over-runs or unexpected changes in commodity prices could render any future development uneconomic notwithstanding positive results from one or more feasibility studies, which would have a material adverse effect on the Company’s business, financial condition, results of operations and prospects. For a more comprehensive overview of the risks related to Discovery Energy Metals’ business, readers should review the Company’s continuous disclosure documents filed under its profile at www.sedarplus.ca.

Forward-Looking Statement Disclaimer: Statements in this article regarding Discovery Energy Metals’ potential for major discoveries, future stock-price appreciation, and project advancement are forward-looking statements within the meaning of applicable Canadian and U.S. securities laws. Actual results may differ materially. Factors that could cause results to differ include metal-price volatility, exploration failures, permitting issues, financing risks, dilution from future equity issuances, changes in regulatory environment, and general economic conditions. Statements about the copper market (supply deficits, forecast prices, and M&A patterns) are based on third-party forecasts from the analysts, agencies, and publications cited above, each of which contains its own assumptions and its own risks; none of those forecasts is a guarantee of outcome.

Compensation Disclosure: This article was produced as part of a public awareness campaign hired by the issuer. Full details are available under the heading “Public Awareness Campaign” below, including total compensation amount and payment structure.

This website is not a broker, dealer, investment or financial advisor and does not purport to be one. All information contained herein is for informational purposes only and should not be construed as an offer to buy or sell any security of any kind. Information is provided on an equal basis to all readers, intended for a general audience, with no adjustment bias or personalization to any individual’s personal financial situation whatsoever.

Forward Looking Statements

Information provided herein contains forward-looking statements. Any statements that express or involve discussions with respect to opinions, predictions, expectations, beliefs, plans, projections, goals, assumptions, future events, future performance, estimations or prophecies are not statements of historical facts and may be forward-looking statements, and thus may be unable to be relied upon. The forward-looking statements contained herein are based on personal opinions of estimates and projections resulting in personal expectations at the time the statements are made that may involve a number of risks and uncertainties which could cause actual results or events to materially differ from those presently anticipated or opined herein. Forward-looking statements may be identified through the use of words such as, but not exclusively, “expects,” “will,” “anticipates,” “estimates,” “believes,” or statements indicating, but not limited to, certain actions such that “may,” “could,” “should,” or “might” occur.

DEMC-Specific Forward-Looking Statements Disclaimer

This article contains certain information, forecasts, projections, and/or disclosures about Discovery Energy Metals Corp. (the “Company”) and its prospects that may constitute “forward-looking information” and “forward-looking statements” under applicable Canadian securities laws (collectively, “forward-looking statements”). All such statements, forecasts, projections and/or disclosures included in this article, other than those of historical fact, that address activities, events or developments that the Company anticipates or expects may or will occur in the future (in whole or in part) should be considered forward-looking statements.

Forward-looking statements are based upon the Company’s current internal expectations, internal estimates, internal projections and internal assumptions about future events and trends that management believes may affect the Company’s financial condition, operations, business strategy and financial needs. The forward-looking statements are subject to significant known and unknown risks, uncertainties and other factors, many of which are beyond the control of the Company. Forward-looking statements can be identified by the use of forward-looking terminology such as “expect,” “likely,” “may,” “will,” “should,” “intend,” “anticipate,” “potential,” “proposed,” “estimate,” “believe,” “plan,” “forecast” and other words of similar import, including negative and grammatical variations thereof, or statements that certain events or conditions “may” or “will” happen, or by discussions of strategy. Actual results and developments may differ materially from those contemplated by these forward-looking statements. Forward-looking statements include, but are not limited to, statements with respect to raising funds from investors; the use of net proceeds of any investment; the Company’s business objectives and the anticipated timing of execution; the expected performance of the Company’s business and operations; the Company’s ability to expand and develop its operations; expectations regarding the Company’s revenues, expenses and profits; the competitive conditions of the mining industry; the Company’s anticipated obligations to comply with safety and regulatory matters related to the mining industry; the effect of any new or altered government regulations with respect to the mining industry; the grant or renewal of licenses or governmental approvals required to conduct activities related to the Company’s business; the Company’s ability to maintain permits and approvals required to operate effectively; the intentions of management of the Company; the Company’s expectations that third parties will fulfill their obligations; the Company’s ability to retain and attract key personnel; the Company’s ability to raise additional funds; future liquidity and financial capacity; the Company’s ability to manage cash flows; the Company’s plan with respect to any payments of dividends, if any; the Company’s possible exposure to liability relating to the mining industry; and contractual obligations and commitments.

Public Awareness Campaign

Discovery Energy Metals Corp. (CSE: DEMC) has engaged ClickCatalyst Inc. to conduct a 60-day public-awareness campaign commencing May 27th, 2026, in exchange for total cash compensation of CAD $250,000 (CAD $100,000 paid up front, with the CAD $150,000 balance payable during the engagement), in connection with the preparation and distribution of communications consisting of publicly available corporate information about the Company, distributed through Capital Rankings.

Limitation of Information

The information we provide represents only a small amount of information regarding the Company and is not sufficient to formulate an investment decision. As such, that information should only be a starting point from which you conduct an in-depth investigation of the company from available public sources, such as sedarplus.ca, otcmarkets.com, sec.gov, google.com and other available public sources, as well as consulting with your financial professional, investment adviser, and/or registered representative with a registered securities broker-dealer. The website is not liable for any investment decisions by its visitors, readers or subscribers. Investors are cautioned that they may lose all or a portion of their investment and should independently conduct their own research and arrive at their own decisions or consult with a qualified and registered broker, investment adviser or financial adviser.

Property Interest Notes

Discovery Energy Metals holds a 100% interest in the Crystal Lake Copper-Molybdenum Property (BC) subject to the acquisition terms and contingent payments described in the Crystal Lake acquisition PR dated June 17, 2025, including a 2% Net Smelter Returns royalty to Zimtu Capital Corp. (with a 1% buyback right for CAD $1,000,000 within five years). Discovery Energy Metals holds a 45% joint-venture interest in the Koster Dam Project (BC); Cariboo Rose Resources Ltd. holds the remaining 55% and is the initial managing operator. Discovery Energy Metals holds the ESN Project (Nevada) via its ISM Resources Corp. subsidiary, subject to a 2% Net Smelter Returns royalty to Trend Resources LLC and a 2% Net Smelter Returns royalty to Emigrant Springs Gold Corporation (both with 1% buyback rights at USD $1,000,000 per 1% within five years). Discovery Energy Metals’ Québec properties are subject to standard Québec mineral-claim renewal and expenditure obligations. There are no mineral resources or mineral reserves on any of Discovery Energy Metals’ properties, which are early-stage exploration projects. There can be no assurances that any of these projects will be developed commercially or at all.

Non-Arm’s-Length Relationships (Disclosed)

Colton Griffith, a director of Discovery Energy Metals Corp., is Marketing Manager at Zimtu Capital Corp., the vendor of the Crystal Lake Copper Property. Mr. Griffith abstained from Discovery Energy Metals board resolutions approving the Zimtu acquisition agreement. Jody Bellefleur serves as Chief Financial Officer of both Discovery Energy Metals Corp. and Zimtu Capital Corp. and also serves as Chief Financial Officer of Q2 Metals Corp. (TSXV: QTWO). These related-party relationships are disclosed in the applicable Discovery Energy Metals issuer press releases and MD&A filings and are summarized here for reader convenience.

Qualified Persons

The technical information in this article relating to the Crystal Lake Copper Property was previously reviewed and approved by Nicholas Rodway, P.Geo. (EGBC #46541), an independent “Qualified Person” as defined by National Instrument 43-101 — Standards of Disclosure for Mineral Projects. The technical information relating to the Koster Dam Project was previously reviewed and approved by Geoffrey Goodall, P.Geo. (Global Geological Services Inc.), the author of the Koster Dam NI 43-101 Technical Report dated February 20, 2023. The technical information relating to the ESN Project was previously reviewed and approved by Bradley C. Peek, MSc, CPG, the author of the ESN NI 43-101 Technical Report dated March 1, 2022. Investors are cautioned that grab samples are selective by nature and may not represent in-situ grade or tonnage.

Disclaimers Applicable to Third Party Properties

This content and related maps contain information about adjacent properties and properties with similar characteristics on which the Company has no right to explore or mine. Readers are cautioned that mineral deposits on adjacent properties or properties that share similar characteristics are not indicative of mineral deposits on the Company’s properties. Specifically: information referenced in this article about the KGHM Robinson Mine, the Battle Mountain gold trend, the Bald Mountain gold mine (Kinross Gold), the former-producing Blackdome gold-silver mine, Foran Mining Corporation (TSX: FOM) and its acquisition by Eldorado Gold, and comparable copper-focused M&A transactions referenced herein (BHP/Oz Minerals, BHP-Lundin/Filo Corp, Hudbay/Arizona Sonoran, South32/Arizona Mining, Glencore/Teck Coal, Anglo American/Teck Resources) is provided for informational and contextual purposes only, has not been verified by the Company or its Qualified Persons, and is not indicative of mineralization or commercial outcome on any Discovery Energy Metals property.

Trading involves significant risk of loss and is not suitable for all investors. You should carefully consider your investment objectives, level of experience, and risk appetite before making a decision to trade. Most importantly, do not invest money you cannot afford to lose.

STREETWISE | JAMES MACKINTOSH

An Objective Study: The Surprising Returns of Canadian Mining Portfolios

Junior Miners Regain Momentum as Gold Stays Elevated & Copper Demand Broadens

How to Make Billions Buying the Same Things Everyone Else Does

North American Mining Reset: Market Impact & Why Canadian Juniors May Be Next

Podcast

Your personal-finance and career checklist.